Equinix

2025-09-24 Equinix, Inc. (NASDAQ:EQIX) Magnar Tan

Executive Summary

Equinix, Inc. (NASDAQ: EQIX) is the global leader in digital infrastructure, operating over 260 data centers in 75+ major metro areas. It provides mission-critical interconnection and cloud services to more than 10,000 customers including hyperscale cloud providers and enterprises. In 2024, the company reported solid financial growth and increased capital spending towards doubling its data center capacity by 2029 with a strong focus on AI-optimised infrastructure.

Notably, Equinix’s share price experienced a steep decline in 2025 amid broader market volatility and investor concerns over macroeconomic factors and rising capital expenditures. Despite this, the company’s operational fundamentals remain robust, supported by secular tailwinds from cloud adoption and AI-driven digital transformation. Equinix continues making strategic investments in global ecosystems and sustainability, positioning itself for long-term growth in the digital economy.

1. Company Overview

Equinix, Inc. provides network-neutral data center services for cloud and information technology services providers, content providers, financial companies, enterprises, and network and mobility services providers. Equinix’s Platform encompasses a network of International Business Exchange (IBX) and xScale data centers strategically located in key markets across the Americas, Asia-Pacific, and Europe, the Middle East, and Africa. As of December 31, 2024, the company served over 10,000 customers including telecommunications carriers, cloud and IT service providers, digital media companies, financial services firms, and global enterprises.

1.1 Business Segments

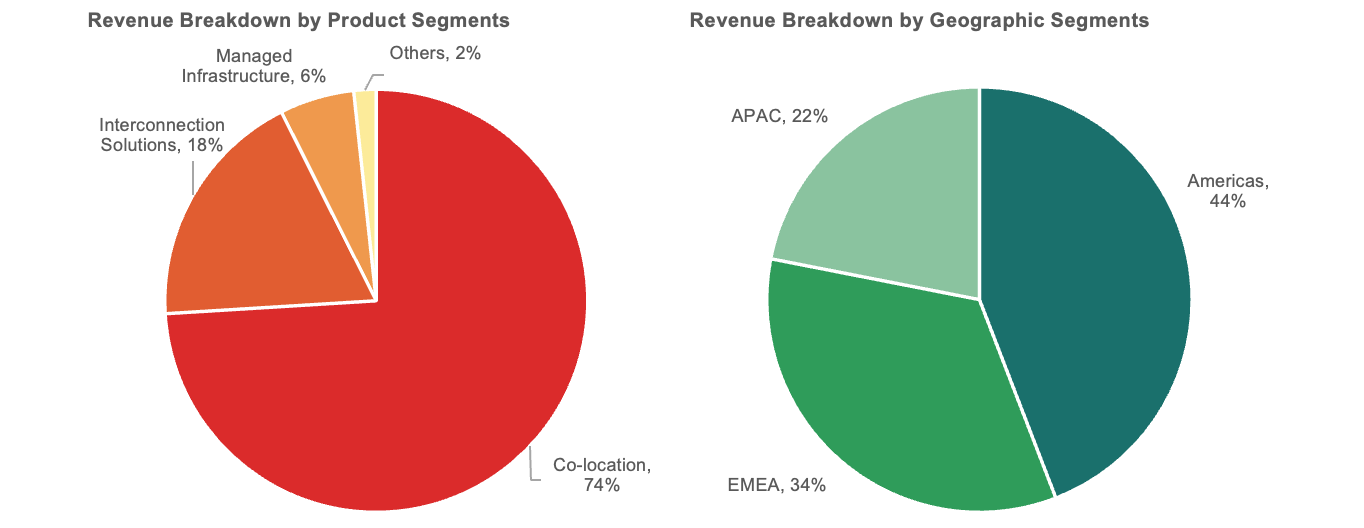

Equinix’s offerings are classified into four main product categories: Colocation, Interconnection, Managed Infrastructure, and Others.

Colocation: licensing of cabinet space and power, with products such as Private Cages, Secure Cabinets, and Secure Cabinet Express. Colocation services enable customers to house their IT infrastructure in Equinix’s data centers, facilitating faster digital transformation and deployment. In FY2024, the Colocation category reported revenue of US$6,058 million, which accounted for 74% of the company’s revenue.

Interconnection solutions: connects businesses directly and securely within and between Equinix data centers. Key offerings include Equinix Fabric, Equinix Internet Exchange, and Equinix Cross Connects, which facilitate efficient connectivity and data exchange among customers and partners. In FY2024, the Interconnection solutions reported revenue of US$1,519 million, which accounted for 18.6% of the company’s revenue.

Managed Infrastructure: provides flexible managed platforms for cloud, storage, backup, and firewall services. Managed infrastructure solutions leverage hybrid and multi-cloud experiences, allowing organisations to focus on their core business functions while Equinix manages their IT infrastructure. In FY2024, the Managed Infrastructure reported revenue of US$467 million, which accounted for 5.7% of the company’s revenue.

Others: Includes revenues from leasing and hedging activities, contributing to the overall financial performance of the company. In FY2024, the Other category reported revenue of US$140 million, which accounted for 1.7% of the company’s revenue.

Equinix operates through three primary business segments, which are categorised based on geographic regions: Americas, EMEA (Europe, the Middle East, and Africa), and Asia-Pacific. The company’s global footprint, consisting of 268 data centers across 35 countries and 74 markets. In FY20204, Americas accounted for 44.1% of the company’s revenue, followed by EMEA (33.9%), and Asia-Pacific (21.9%).

Equinix also categorises its revenue by recurring (94%) and non-recurring revenue (6%):

Recurring revenue: comprises of colocation and interconnection and managed infrastructure offerings. Customers are typically billed on a fixed, recurring basis each month for the duration of their contract, generallly one to five years in length.

Non-Recurring revenue: derived from fees charged from installations related to a customer’s initilal deployment and professional services performed for customers. They are typically billed once upon completion of the service.

1.2 Revenue Drivers

Continued expansion of Equinix’s global data center footprint: Expansion is the main driver of Equinix’s revenue growth. Both recurring and non-recurring revenues fundamentally rely on the company’s success in expanding its data center capacity, entering new markets, and attracting additional customers.

Recurring revenue streams like multi-year contracts for colocation and interconnection form the predictable base, but their growth depends on winning new customers and increasing the footprint of existing ones. As Equinix expands with new facilities and taps into emerging markets such as Southeast Asia, it creates more opportunities for fresh contracts and higher usage among current clients, driving up total recurring revenue.

Non-recurring revenue, which includes one-time installation, set-up, and project-based fees, is likewise intrinsically linked to expansion. Most of this revenue is generated when onboarding new customers or deploying new infrastructure for existing ones, especially during periods of rapid market entry, network upgrades, or the launch of new data center sites. Without continued expansion of customer relationships and geographic reach, non-recurring revenue would diminish.

Increased demand from digital transformation, cloud, and AI adoption: more than half of the volume of Equinix’s top 25 deals in Q4 2024 were for high-performance compute and AI workloads, and they expect this secular trend to drive sustained demand for additional space, power, and interconnection across their network. Management explicitly mentions growing revenue from existing customers as a contributing factor, noting that over 90% of recurring booking growth comes from upselling and expanding with current clients. This focus on helping customers scale further within their ecosystem, aided by interconnection density and new product offerings is another driver of revenue.

1.3 Cost Drivers

Capital Expenditures for Expansion and Development: A significant portion of costs stem from active investments in expanding the global footprint through new data centers, acquisitions, and upgrades. Capital investment represents a major ongoing cost as Equinix builds new data centers and expands existing ones to support growth, especially AI and cloud-related infrastructure requirements. The company’s capex was approximately $3.0 billion in 2024 and is forecast to increase to $4-5 billion annually by 2027, reflecting an aggressive expansion strategy.

Energy and Cooling Costs (in Cost of Revenues): Data centers consume massive amounts of electricity for both operations and cooling. In 2024, Equinix’s power and cooling costs constituted a significant portion of its operating expenses. Cooling alone can account for up to 40% of total electricity use in some facilities. Equinix manages this through energy efficiency programs and renewable energy purchases but continues to face variability due to regional energy prices and regulatory environments.

Facility Operations and Maintenance (in Cost of Revenues): Costs associated with staffing, repairs, security, and maintaining 24/7 operations across its global footprint constitute another core expense. Employee-related costs including wages, benefits, and stock-based compensation add materially to total operating expenses. In 2024, these operational costs were a substantial contributor to overhead alongside facility lease and maintenance costs.

2. Competitor Analysis

2.1 The Global Data Center and Digital Infrastructure Sector

Rapid Growth Driven by Digital Transformation: Enterprises and hyperscalers are driving rising demand for colocation services, with the colocation market valued at approximately USD 73 billion in 2024, projected to grow at a CAGR of 12-14% over the next five years due to increasing adoption of cloud computing, AI workload, and edge computing.

Cloud and Hyperscale demand: Hyperscale cloud operators dominate capacity demand globally, driving unprecedented investment in large-scale high-density data centers. Industry reports highlight AI-driven data center CapEx expected to exceed USD 500 billion by 2027, with a significant portion directed toward colocation providers.

Sustainability and Energy Efficiency: Data centers today consume about 1% of global electricity, with rising regulatory and public pressure on operators to reduce carbon footprints and improve energy efficiency. Industry partners are increasingly committing to renewable energy, and carbon neutrality.

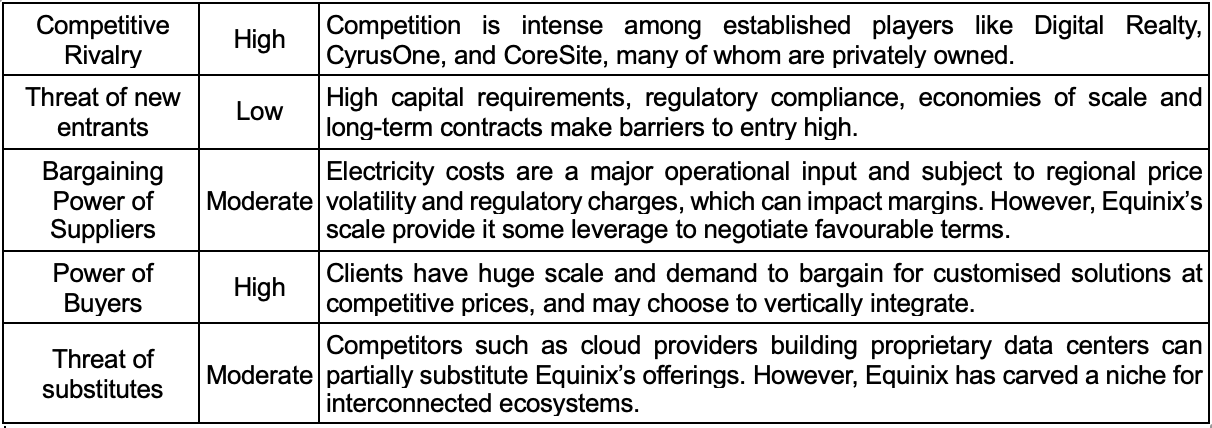

2.2 Porter’s Five Forces Analysis

2.3 Equinix’s competitive positioning

Global scale and geographic reach: Equinix operates the largest network of interconnected data centers globally, providing unparalleled access worldwide.

Dense interconnection ecosystem: Over 480,000 cross connection creates a unique platform that facilitates seamless integrations, locking in customers and increasing switching costs.

Strategic partnerships and high recurring revenue: Long-term joint ventures and contracts with hyperscale cloud leaders drive steady and predictable high-margin revenues.

3. Investment Thesis

3.1 Sustained Competitive advantage via Network Effects

Hosting over 10,000 customers, including top hyperscalers, cloud providers, and financial institutions, the platform generates strong network effects that increase value as more participants join. This ecosystem creates high switching costs because the operational complexity of replicating such interconnected infrastructure is prohibitive, fostering exceptional customer retention rates consistently above 95 percent. Furthermore, interconnection revenues command high margins estimated around 70 percent and have been growing faster than core colocation revenues, composing roughly one-fifth of recurring revenue. This leads to a predictable revenue base with over 94 percent of total revenues coming from recurring streams, which enhances cash flow stability and supports a premium valuation.

3.2 Prime beneficiary of growth in AI and digital infrastructure

The widespread adoption of hybrid and multi-cloud strategies by enterprises requires secure, low-latency connectivity between on-premises systems and public clouds, directly aligning with Equinix’s core interconnection service. Additionally, the rise of AI workloads, which demand distributed computing resources located near data sources and end users, positions Equinix’s broad footprint of more than 270 AI-ready data centers in over 75 metropolitan markets as a necessary infrastructure backbone. Global data sovereignty regulations further strengthen demand for providers with extensive geographic coverage such as Equinix. The company’s commitment to increase capital expenditures to $4 to 5 billion annually through 2029, with plans to double its data center capacity, underscores its preparedness to invest in high-density, AI-optimised facilities. This strategic alignment with secular trends supports a growth narrative that justifies premium financial multiples and positions Equinix favorably among growth-oriented investors.

4. Valuation

Peer comparison reveals that Equinix is trading at a premium valuation multiple, reflecting its leadership in the industry attributed to its high-quality asset base, durable cash flows and unique global scale. The 22x multiple used is consistent with multiples observed among top-tier global data center and digital infrastructure REITs. Using a Multiple Based Valuation method, I calculated target price based on EV/EBITDA and P/AFFO I arrived at a blended target price of $994.53 for 2027 and $1,190.97 for 2029. This represents a 25.8% and 50.7% upside respectively.

5. ESG Assessment

Equinix holds an MSCI ESG rating of AAA and has been recognised by CDP with an “A” for climate leadership for three consecutive years. In 2024, Equinix further advanced its “Future First” strategy, focusing on responsible growth in digital infrastructure and operational excellence across all three ESG pillars.

(Environmental) Decarbonisation, Energy, and Water Management: Equinix operates one of the world’s largest and most energy-intensive data center portfolios. In 2024, the company achieved 96% renewable energy coverage for the seventh consecutive year and executed 370 MW of new power purchase agreements, including first-in-market deals in APAC. Its average annual PUE (Power Usage Effectiveness) improved to 1.39, reflecting ongoing investment in energy efficiency and innovation. Equinix is advancing science-based greenhouse gas emissions reductions, reporting an absolute 24% reduction in operational emissions against its 2019 baseline, despite significant portfolio expansion. Water management has become increasingly important; Equinix achieved portfolio-wide WUE (Water Usage Effectiveness) of 0.95 and launched a Water Focus Program to drive best practices in cooling water use.

(Social) Digital Inclusion, Workforce Diversity, and Health and Safety: Social priorities at Equinix are centered on bridging the digital divide, fostering belonging and inclusion, and delivering industry-leading reliability and safety. In 2024, employees volunteered 37,695 hours across 63 organisations, and the company donated $4.1 million towards digital inclusion and community causes. Diversity metrics show 28% women in the workforce and 35% at the VP level and above. Equinix averaged 51 hours of training per employee. Health and safety outcomes remain strong, with a recordable injury rate of 0.07 per 200,000 hours and no work-related fatalities.

(Governance) Strong Ethical Oversight and Risk Management: Equinix’s governance emphasises board independence, transparency, and stakeholder engagement. Seven out of nine board directors are independent, and sustainability strategy is regularly overseen by dedicated board and executive committees. The company is globally ISO 22301 certified for business continuity and adheres to leading anti-corruption and privacy standards. All employees and board members complete annual ethics, code-of-conduct, and anti-bribery training. Equinix has also emerged as one of the leading issuers of green bonds among U.S. corporates, raising over $7 billion to date for sustainable financing.

6. Risks and Mitigation

Data center oversupply: Data center building occurs when there is high demand and presence of offtakers. However, construction could take years and demand might plateau along the way if AI capabilities fail to live up to its expectations.

Dependence on hyperscalers: A large demand in the data center sector is primarily driven by hyperscalers. There is a risk that hyperscalers may opt to move their data servers in-house. However, the average lease maturity for the company is greater than 20 years, with very few leases expiring in the near future.

Rising interest rates: Currently, data center REITs are able to raise funds for expansion and development at relatively low rates. The majority of cash flow is used to pay dividends and fund capital expenditures. If interest rates rise, the borrowing costs and significant debt balances would likely need to be financed or refinanced at higher rates. Furthermore, the attractiveness of data center REITs as dividend yield investments might decline in a rising rate environment.